I am starting to be market-neutral (maybe I want to fight against the market and have a small-net short position) and dollar bullish again.

Edit:

The risk/reward for the long SEK and short yen positions seem to be deteriorating

maybe positions with long positions in CAD or USD now.

I was kind of bearish on oil but I didn't declare a position on it last week when it was near a high. damn...

Tuesday, March 31, 2009

Thursday, March 26, 2009

The disaster of "consensus investing"

Early March Saw Largest Increase In Short Interest In 9 Months

I didn't perfectly time the "bear market rally," but I was bearish before I started the "real-time experiment" (basically what George Soros did in the Alchemy of Finance without any money)... but Zero Hedge points out that there was a large increase in short positions between 3/2/09 and 3/13/09. Remember, it is a bad time to short when most people are doing it and when everyone is already bearish. I suppose metagame and game theory considerations are important when investing/trading/speculating. I did not want to be net-short during early March because it seems a rally would be a realistic possibility.

Right now, I suppose there is enough bullish sentiment and enough people disagreeing with my views to allow me to be net-short in the US equity markets with a moderate risk/reward profile.

Remember, you always have to question yourself and attempt to falsify your own views.

I didn't perfectly time the "bear market rally," but I was bearish before I started the "real-time experiment" (basically what George Soros did in the Alchemy of Finance without any money)... but Zero Hedge points out that there was a large increase in short positions between 3/2/09 and 3/13/09. Remember, it is a bad time to short when most people are doing it and when everyone is already bearish. I suppose metagame and game theory considerations are important when investing/trading/speculating. I did not want to be net-short during early March because it seems a rally would be a realistic possibility.

Right now, I suppose there is enough bullish sentiment and enough people disagreeing with my views to allow me to be net-short in the US equity markets with a moderate risk/reward profile.

Remember, you always have to question yourself and attempt to falsify your own views.

Wednesday, March 25, 2009

Status of the real-time experiment

I think I lost about 5-6% of the hypothetical portfolio in March largely because of the Federal Open Market Committee anouncement in March 18 that caused the dollar to fall and bonds to rise when I was bullish on the dollar and bearish on treasuries respectively.

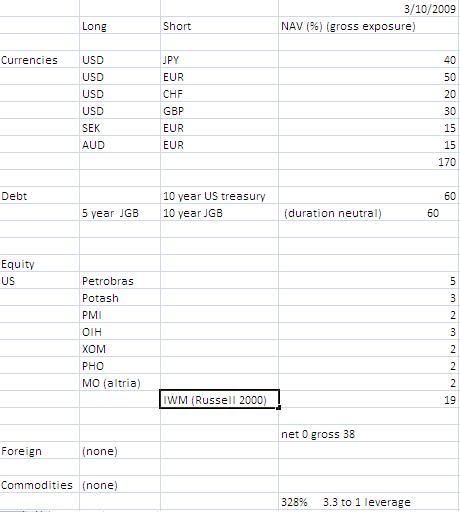

See this for positions as of 3/10/09:

I was right, however, in my bullish views of the Swedish Krona and Australian Dollar, and my bearish views of the Japanese yen but those positions weren't large enough to offset the large dollar positions. Also, the equity longs did well for the general bear market rally. There was no commodity exposure except in the form of some equity selections.

Equities:

See march 10 list for longs

short russell 2000 and S&P 500 indices

(net short 10% of nav) (will increase if it market rallies strongly)

Debt:

short 10 year Japanese government bond (not steepening trade) (60% nav)

(my reasoning is that Japanese savings rate is falling so they would not be able to finance any deficits... also economic recovery would drive up interest rates too. risks include government QE)

Commodities:

long gold (5% of nav) writing covered calls for $1000

currencies:

generally bullish on SEK/ bearish on yen (although short-yen exposure is best expressed with the short JGB position)

I am somewhat agnostic on EUR and USD now

See this for positions as of 3/10/09:

I was right, however, in my bullish views of the Swedish Krona and Australian Dollar, and my bearish views of the Japanese yen but those positions weren't large enough to offset the large dollar positions. Also, the equity longs did well for the general bear market rally. There was no commodity exposure except in the form of some equity selections.

Equities:

See march 10 list for longs

short russell 2000 and S&P 500 indices

(net short 10% of nav) (will increase if it market rallies strongly)

Debt:

short 10 year Japanese government bond (not steepening trade) (60% nav)

(my reasoning is that Japanese savings rate is falling so they would not be able to finance any deficits... also economic recovery would drive up interest rates too. risks include government QE)

Commodities:

long gold (5% of nav) writing covered calls for $1000

currencies:

generally bullish on SEK/ bearish on yen (although short-yen exposure is best expressed with the short JGB position)

I am somewhat agnostic on EUR and USD now

Monday, March 23, 2009

Arguments against equities

Some arguments I have against equities (I do not have enough time to edit these):

Nominally, I think the bottom would be around 350-500. But, I do expect the general equity market to have higher dividend yields as this reflects increased discounting by the general population. I expect dividend yields for the general market to be at least 200 bp higher than 10 government year bonds as the market because less liquid as there would be less market participants (so stocks would also have a "liquidity premium"). I also expect the market would not price in economic growth too and the 200 bp number will also be applied to companies with solid cash flow and little debt. Those companies might lose nominal value in the future, but of course, they would outperform others. In addition, a sell-off of dollar denominated fixed income assets would also lower prices as this drives up yields and exacerbate deflation further. I do not expect a level of sub 100 because unlike the NASDAQ bubble, many of these companies do something for cash flow, and I do expect many of the companies removed by the Darwinian flush to be delisted and replaced with stronger companies.

But the best answer for when the bottom would occur would be in the form of a rhetorical question without an immediately quantifiable answer, and one has to consider game theory considerations such as looking at VIX and the put/call ratio which provide information about market participants' sentiment. The biggest question one has to answer is when the Darwinian flush of the equity markets would finish. This is not a question of intrinsic value (as stocks are not solely valued on valuation, but on discounted cash flow according to the standard Gordon model), but again a large part is based on people's time preferences. Since people do not save as much in the US, the discounting rates would be higher than in the Japanese deflation which would have a stronger short term effect on stock prices causing the decline to be quicker. Also, in Japan, these was less labor competition and securer jobs after the asset bubble burst which is another reason for increased discounting. The deflationist paradigm has help those who embraced it understand this crisis. Another way to ask is to question when would everyone realize that "buy and hold" may work for some people (such as Warren Buffett), but does not work for everyone? When people start realizing that equities have downward volatility in long run as well as the short-run as evidenced by the Japanese equity market for the last two decades? When do people who are saving for education, housing, and retirement leave the equity market (in a way similar to a Darwinian flush) when they realize that “long beta” is a bad “investment” “strategy” as they start demanding liquidity? Even people who are currently bullish (in the long term, not technical traders who go long in anticipation of a bear market rally) on equities argue that if you need liquidity, then do not put money in the stock market. This is the best argument I see for being bullish on equities, but it hasn’t convinced me.

Even that article confirms some of my views:

Fixed-income will be somewhat popular again because the opportunity cost of fixed-income is lower because the return on most assets would be lower and most likely negative. Of course, treasuries are safe (relatively) "nominal assets" were one can get their principal + interest back. (Image a world when the US government defaults... would that be a world that would be investable? ... would it be an "anthropically" possible scenario?) (See Peter Thiel's speech for a discussion about "anthropic investing" although he did not use those terms.) The return on equities would be lower now, and have a negative Sortino ratio (during this bear market), as people suddenly realize that equities are risky. The high nominal return on equities during the last three decades (which some of the gains were erased in the last two years) is partly caused by increased earnings of companies, but a decrease in the equity risk premium, as people who didn't know anything about security analysis bid up the price of stocks. This causes a reflexive process encouraging more people to invest in stocks as it went up in "value" when a large portion of the gains was caused a reduction in the risk premium. Many people seeking liquidity would take money out of the stock market (since they cannot play "for the long run.") The increase in liquidity demand and the epiphany that equities do experience negative volatility causes an increase in the equity risk premium which then causes a decline in equity prices. This might not decrease the "inherent value" of equities, but it would decrease the nominal value. Of course, other factors such as pricing in no dividend growth for years would be priced in causing its price to go down. If one wanted to shun potential nominal volatility (which means protection from negative volatility, but eschewing positive volatility), one would turn to nominal assets such as Treasuries and other bonds. If they have a high-risk tolerance, they might go to municipal or corporate bonds instead of Treasuries.

Nominally, I think the bottom would be around 350-500. But, I do expect the general equity market to have higher dividend yields as this reflects increased discounting by the general population. I expect dividend yields for the general market to be at least 200 bp higher than 10 government year bonds as the market because less liquid as there would be less market participants (so stocks would also have a "liquidity premium"). I also expect the market would not price in economic growth too and the 200 bp number will also be applied to companies with solid cash flow and little debt. Those companies might lose nominal value in the future, but of course, they would outperform others. In addition, a sell-off of dollar denominated fixed income assets would also lower prices as this drives up yields and exacerbate deflation further. I do not expect a level of sub 100 because unlike the NASDAQ bubble, many of these companies do something for cash flow, and I do expect many of the companies removed by the Darwinian flush to be delisted and replaced with stronger companies.

But the best answer for when the bottom would occur would be in the form of a rhetorical question without an immediately quantifiable answer, and one has to consider game theory considerations such as looking at VIX and the put/call ratio which provide information about market participants' sentiment. The biggest question one has to answer is when the Darwinian flush of the equity markets would finish. This is not a question of intrinsic value (as stocks are not solely valued on valuation, but on discounted cash flow according to the standard Gordon model), but again a large part is based on people's time preferences. Since people do not save as much in the US, the discounting rates would be higher than in the Japanese deflation which would have a stronger short term effect on stock prices causing the decline to be quicker. Also, in Japan, these was less labor competition and securer jobs after the asset bubble burst which is another reason for increased discounting. The deflationist paradigm has help those who embraced it understand this crisis. Another way to ask is to question when would everyone realize that "buy and hold" may work for some people (such as Warren Buffett), but does not work for everyone? When people start realizing that equities have downward volatility in long run as well as the short-run as evidenced by the Japanese equity market for the last two decades? When do people who are saving for education, housing, and retirement leave the equity market (in a way similar to a Darwinian flush) when they realize that “long beta” is a bad “investment” “strategy” as they start demanding liquidity? Even people who are currently bullish (in the long term, not technical traders who go long in anticipation of a bear market rally) on equities argue that if you need liquidity, then do not put money in the stock market. This is the best argument I see for being bullish on equities, but it hasn’t convinced me.

Even that article confirms some of my views:

"If you need a certain amount of cash within a 3-5 year time period, it cannot be in stocks. The vagaries of stock prices on a five year basis are unknowable, but history tells us that prices usually revert to fair value over five year periods. For example, if you need money for a down payment on a home, tuition payment, or emergency, that money cannot be in stocks. It must be in cash or bonds. If you are in retirement and drawing from your portfolio for living expenses, you must have a certain allocation in bonds or cash to fund current needs"

Fixed-income will be somewhat popular again because the opportunity cost of fixed-income is lower because the return on most assets would be lower and most likely negative. Of course, treasuries are safe (relatively) "nominal assets" were one can get their principal + interest back. (Image a world when the US government defaults... would that be a world that would be investable? ... would it be an "anthropically" possible scenario?) (See Peter Thiel's speech for a discussion about "anthropic investing" although he did not use those terms.) The return on equities would be lower now, and have a negative Sortino ratio (during this bear market), as people suddenly realize that equities are risky. The high nominal return on equities during the last three decades (which some of the gains were erased in the last two years) is partly caused by increased earnings of companies, but a decrease in the equity risk premium, as people who didn't know anything about security analysis bid up the price of stocks. This causes a reflexive process encouraging more people to invest in stocks as it went up in "value" when a large portion of the gains was caused a reduction in the risk premium. Many people seeking liquidity would take money out of the stock market (since they cannot play "for the long run.") The increase in liquidity demand and the epiphany that equities do experience negative volatility causes an increase in the equity risk premium which then causes a decline in equity prices. This might not decrease the "inherent value" of equities, but it would decrease the nominal value. Of course, other factors such as pricing in no dividend growth for years would be priced in causing its price to go down. If one wanted to shun potential nominal volatility (which means protection from negative volatility, but eschewing positive volatility), one would turn to nominal assets such as Treasuries and other bonds. If they have a high-risk tolerance, they might go to municipal or corporate bonds instead of Treasuries.

My market view

http://seekingalpha.com/article/127105-10-reasons-why-we-still-haven-t-hit-bottom?source=article_sb_popular

I like that article as it states what is obvious to me, but I hate it when most investors agree with me. It makes it harder to understand the metagame if everyone thinks like you. Jim Rogers says that consensus investing is a disaster, and of course, empirical evidence confirms this. I am also a Popperian that attempts to falsify my own beliefs.

I think I should re-enter small short equity indices positions in the US and Europe. 15-20 percent net short exposure using indices (S&P 500 and Russell 2000 mix with a bias for s&P 500) in the hypothetical portfolio. S&P 500 is at 823 today, and it might go up to 9000. 8400-8500 might be the actual resistance though. I also should try to remove some of those equity longs except those that have commodity exposure.

Of course, I got burned on bad currency bets (betting that the dollar would strenghten) and bond bets (short 10 year US treasury) in the putative portfolio on March 18 because of the FOMC announcement of quanitative easing. I am now dollar bearish in the short term and would add to the SEK/USD position. I thought the trade deficit would fix itself, but it didn't. Furthermore, an increase in oil prices would exacerbate the trade deficit as traders bid up the price of oil. I think there will be a time (an emphasis on time) to short gold, copper, and

I do not know enough about the European equity market though. I wonder if the strengthen euro is priced in (I need to do more research on the portion of the European economy as exports to the US) or the Eastern European crisis. Too bad I cannot see the IR/NMR peaks on European equities and see the absense of "strengthening Euro" or whatever in their pricing in an attempt to arbitrage the difference between market perception and reality. You never invest on consensus, and I think these things (except perhaps strengthening Euro) are already priced in.

Since the state provides for the people in Europe, I expect lower discount rates among Europeans. I also assume that massive amounts of retirement money hasn't been shoved into European equities so my discounting hypothesis above would not apply in this economy.

The risk/reward for European shorts does not seem compelling, and I have other things to do now besides study the market.

I havent looked at enough on Europe though.

I like that article as it states what is obvious to me, but I hate it when most investors agree with me. It makes it harder to understand the metagame if everyone thinks like you. Jim Rogers says that consensus investing is a disaster, and of course, empirical evidence confirms this. I am also a Popperian that attempts to falsify my own beliefs.

I think I should re-enter small short equity indices positions in the US and Europe. 15-20 percent net short exposure using indices (S&P 500 and Russell 2000 mix with a bias for s&P 500) in the hypothetical portfolio. S&P 500 is at 823 today, and it might go up to 9000. 8400-8500 might be the actual resistance though. I also should try to remove some of those equity longs except those that have commodity exposure.

Of course, I got burned on bad currency bets (betting that the dollar would strenghten) and bond bets (short 10 year US treasury) in the putative portfolio on March 18 because of the FOMC announcement of quanitative easing. I am now dollar bearish in the short term and would add to the SEK/USD position. I thought the trade deficit would fix itself, but it didn't. Furthermore, an increase in oil prices would exacerbate the trade deficit as traders bid up the price of oil. I think there will be a time (an emphasis on time) to short gold, copper, and

I do not know enough about the European equity market though. I wonder if the strengthen euro is priced in (I need to do more research on the portion of the European economy as exports to the US) or the Eastern European crisis. Too bad I cannot see the IR/NMR peaks on European equities and see the absense of "strengthening Euro" or whatever in their pricing in an attempt to arbitrage the difference between market perception and reality. You never invest on consensus, and I think these things (except perhaps strengthening Euro) are already priced in.

Since the state provides for the people in Europe, I expect lower discount rates among Europeans. I also assume that massive amounts of retirement money hasn't been shoved into European equities so my discounting hypothesis above would not apply in this economy.

The risk/reward for European shorts does not seem compelling, and I have other things to do now besides study the market.

I havent looked at enough on Europe though.

Saturday, March 21, 2009

More thoughts on deflation/inflation

To put this in the proper context... it is a response to this post:

http://stefanmikarlsson.blogspot.com/2009/03/return-of-inflation.html

I am still a deflationist (the open market policies are definitely inflation though)... but, of course, political incentives would promote inflationary policies. For example, the Japanese were savers, thus the electorate would be reluctant to see that value of their savings eroded by inflationary monetary policies. Hopefully, Bernanke would simply give up reflationary policies eventually and accept some of the economic and social benefits of deflation. Of course, deflation does cause significant harm for many people, and, hopefully, some government redistributive policies (if competently enacted) would ameliorate some of the pain. Of course, I do want people to feel some pain because it would have a positive deterrent effect on future generations though. Those last statements, of course, reflect my normative desires (which reflect negative utilitarianism), and not my empirical perspective.

I still believe in deflation (and reject the hyperinflationist view point) unless I see wage nominal inflation (even this did not happen when Greenspan enacted his inflationary policies in the early 2000s) and the price of consumer goods (such as cars) go up dramatically. I have thus given the evidence that could falsify my (actually mostly plagiarized from Mish Shedlock, and to a lesser extent Edward Harrison) deflationary thesis in a Popperian fashion. I do not see any macroeconomic trend that would pressure wage growth unless Bernanke literally drops money out of a helicopter, not merely use QE in open market operations as that money would not reach many people.

Also, you did mention the CPI. Of course, most Austrians do not regard that as a reliable measure of inflation (as they are compelling cases for the perspectives it understates or overstates increases or decreases the increase or decrease in the price level) because changes in price level are not inflation, but merely its effects. Even if we do disregard food and energy, I am sure that the some goods in the basket of CPI goods are imported. This could cause a rise in the CPI in a deflationary environment if the imported goods are from a country that does not have a currency pegged to the US dollar (like the renminbi and gulf coast currencies) and if the trade-weighted US dollar index drops which would cause the dollar to drop relative to other floating currencies.

Regarding the recent price increases, it does not falsify deflation as it merely reflects an increase in the velocity of capital after the FOMC announcement. The increase happened because people who had short equity, commodity, bond, and currency positions (relative to the US dollar) had to cover their positions, people entered long positions because of their expectations of Bernanke's reflationary policy and were spooked, and people who were early would anticipate these reactions by other market participants.

http://stefanmikarlsson.blogspot.com/2009/03/return-of-inflation.html

I am still a deflationist (the open market policies are definitely inflation though)... but, of course, political incentives would promote inflationary policies. For example, the Japanese were savers, thus the electorate would be reluctant to see that value of their savings eroded by inflationary monetary policies. Hopefully, Bernanke would simply give up reflationary policies eventually and accept some of the economic and social benefits of deflation. Of course, deflation does cause significant harm for many people, and, hopefully, some government redistributive policies (if competently enacted) would ameliorate some of the pain. Of course, I do want people to feel some pain because it would have a positive deterrent effect on future generations though. Those last statements, of course, reflect my normative desires (which reflect negative utilitarianism), and not my empirical perspective.

I still believe in deflation (and reject the hyperinflationist view point) unless I see wage nominal inflation (even this did not happen when Greenspan enacted his inflationary policies in the early 2000s) and the price of consumer goods (such as cars) go up dramatically. I have thus given the evidence that could falsify my (actually mostly plagiarized from Mish Shedlock, and to a lesser extent Edward Harrison) deflationary thesis in a Popperian fashion. I do not see any macroeconomic trend that would pressure wage growth unless Bernanke literally drops money out of a helicopter, not merely use QE in open market operations as that money would not reach many people.

Also, you did mention the CPI. Of course, most Austrians do not regard that as a reliable measure of inflation (as they are compelling cases for the perspectives it understates or overstates increases or decreases the increase or decrease in the price level) because changes in price level are not inflation, but merely its effects. Even if we do disregard food and energy, I am sure that the some goods in the basket of CPI goods are imported. This could cause a rise in the CPI in a deflationary environment if the imported goods are from a country that does not have a currency pegged to the US dollar (like the renminbi and gulf coast currencies) and if the trade-weighted US dollar index drops which would cause the dollar to drop relative to other floating currencies.

Regarding the recent price increases, it does not falsify deflation as it merely reflects an increase in the velocity of capital after the FOMC announcement. The increase happened because people who had short equity, commodity, bond, and currency positions (relative to the US dollar) had to cover their positions, people entered long positions because of their expectations of Bernanke's reflationary policy and were spooked, and people who were early would anticipate these reactions by other market participants.

Politics and equities

This is a response to this post

I am generally a person with left wing political views. I think it is much more likely for the government to cooperate with the OECD first to crackdown on tax evaders who have money offshore.

Despite my political views, I do not have much optimism in Obama I do expect the markets to go down further and the Bernanke/Obama "reflation" agenda to "fail" (as in not spark new consumer lending or cause stagflation.) I still believe in deflation though, and as the discount rate for long term illiquid assets (stocks are relatively illiquid) rises resulting in investors asking for an increased risk premium for holding onto equities and not pricing in economic growth which would drive down the price of equities, people will liquidate and switch to more liquid assets. They will give up on trying timing the market and profit on a recovery (it probably would not happen anyway) because their discount rates have gone up so they want to protect themselves from nominal short-term losses in assets such as equities. The result is that most people who do not have a long time horizon would not hold on to equities.

So what does this mean? Generally people who hold stocks have more conservative political views and tend to vote Republican. If one lets the process go on untouched, it would result in a shift in a preference for more left-wing policies and a preference for labor over capital since less voting people own stock. But if the government tries to intervene in this natural process (a referrence to the proposal of confiscating IRAs and 401(k)s), they would lose some potential supporters as these people would feel that the government harmed them by confiscating their assets. Thus, it is simply better for the government (if it seeks to generate people with more left-wing views) to let the Darwinian flush in the equity markets to go on unabated and let them relinquish their equities naturally although that would be a painful process for many.

Most people are incompetent at managing their own money and they do realize that now. This incompetence can be explained by the information asymmetries that professional traders have over retail investors, and as explained above, they have higher discount rates during times of crisis which leads them to make bad long-term decisions. I think there will be little resistance to more government involvement in a democratic population now. The people voted for Bush in the last election because the asset bubble in housing and stocks made plenty of people happy despite the economic fundamentals which also explain the tolerance for policies that favor capital over labor.

Thursday, March 19, 2009

Thoughts on the dollar, treasuries, and inflation

Although unusual from my recent ramblings... this post will be more coherent since I wrote it in response to a blog entry from Stefan Karlsson. I saved it because there is a chance that he might delete it.

I thought long-dated bond yields would go up despite a deflationary environment. My reasoning is based on the fact that in a deflationary environment, people generally would move towards liquid assets and relatively shun "duration" exposure so the yield curve would steepen unless the front-end interest rate was high (which is usually the case before a recession). Also, Brad Setser reported increased demand for treasuries by private investors in the 3rd and 4th quarter of 2008. (Setser, to the best of my knowledge did not say anything about the duration preferences of these investors.) I think that this was a one-time maneuver by many investors shifting a large portion of their portfolio into bonds (bond demand would not be financed by a stream of income by private investors) so a large portion of their capital is already exposed to treasury bonds. In addition, foreign demand for long-term treasuries I expected to decrease as government's acknowledge the risk of the "risk-free" long-dated asset (Sester did acknowledge this) and lower trade surpluses in many of the US' trading partners. Lastly, even though private saving would go up, I suppose it would not finance the large deficit as the private sector attempts to deleverages themselves and prefer more liquid shorter-duration exposure. In addition, earning power would decrease so less money would be available for saving which is different from the Japanese scenario. It would seem that the increase in supply for treasuries (especially long-dated) would outstrip an increase in demand if we excluded the printing-press and people suddenly buying bonds after they heard of Bernanke's QE policy (even if there was not sell-off caused by a bursting of the "bond bubble"). I thought Bernanke would result to using QE eventually, but I actually expected yields to go up during the bear market rally.

I did expect the dollar to rise against the euro because it is the world's reserve currency and the world is highly levered in the world's reserve currency so this would increase the demand for dollars during deleveraging. But once the deleveraging was over, the dollar would resume its fall. In addition, the eastern european exposure to the euro would cause significant stress to the currency regime and maybe lower euro interest rates in an attempt to "stimulate" the economy. Also, I erroneously thought that the US trade deficit would narrow (it did), but the latest trade data showed that exports declined more relative to the decline in non-petroleum imports.

Of course, in the future, there is a non-trivial chance that the velocity of money would dramatically accelerate. This would cause inflation or hyperinflation (as defined by an increase in prices), not simply increases in the money supply although that might be the catalyst to trigger such an increase. Of course, inflation and hyperinflation do have a reflexive component to it, and since people believe that the Fed will cause inflation, as it did by increasing the money supply, it drives gold prices up as people seek "real" exposure, not "nominal" exposure. Gold prices do not measure directly inflation as there was positive inflation in the 90's yet lower gold prices as people wanted exposure to assets (or "delusion" in the case of most dot-coms). It measures some derivative of the demand for "real" exposure relative to "nominal" exposure which would increase during times of both deflation and in some inflationary environments. In a deflationary environment, "nominal" low-duration exposure might not offer significant interest, so the opportunity cost for holding gold would be lower. This is one reason why gold could rise in a deflationary environment.

I do not think "reflation" will "work" (which I'll define as producing "desired results" not merely producing inflation.) Even if banks become well-capitalized when the government monetizes their assets, it would not spur "enough" lending because the demand for lending would decrease. While Bernanke can lower the interest on interest-bearing assets by intervening in the bond market by buying agencies and government debt, it would not necessarily lower the "spread" or risk premium for those type of debts and consumer loans. The spread, of course, needs to compensate for the risk in the loans the banks make. I expect a situation similar to that of Japanese banks if the banks are to become well-capitalized. It seems that Bernanke's goals for QE is to lower the interest rates for consumers to get loans rather than recapitalization of banks although the latter is means for the former. I do not think QE will achieve this end. QE might not necessarily cause inflation in a given nation if it is not invested in a the country (in Japan, it might be used for "carry trades" in other currencies) or if the excess money was withdrawn from the money supply after it recapitalized the banks (which happened in Japan according to the figure here).

I still like the deflationist thesis and "Mish" (and not Peter Schiff) made me consider the merits of Austrian empirical economics, although I do not like some Austrian normative economics. Regardless of "deflation" and "inflation," this is an environment characterized by hoarding not entrepreneurialship... who knows whether it will be cash when the velocity of money is low, or real assets.

I thought long-dated bond yields would go up despite a deflationary environment. My reasoning is based on the fact that in a deflationary environment, people generally would move towards liquid assets and relatively shun "duration" exposure so the yield curve would steepen unless the front-end interest rate was high (which is usually the case before a recession). Also, Brad Setser reported increased demand for treasuries by private investors in the 3rd and 4th quarter of 2008. (Setser, to the best of my knowledge did not say anything about the duration preferences of these investors.) I think that this was a one-time maneuver by many investors shifting a large portion of their portfolio into bonds (bond demand would not be financed by a stream of income by private investors) so a large portion of their capital is already exposed to treasury bonds. In addition, foreign demand for long-term treasuries I expected to decrease as government's acknowledge the risk of the "risk-free" long-dated asset (Sester did acknowledge this) and lower trade surpluses in many of the US' trading partners. Lastly, even though private saving would go up, I suppose it would not finance the large deficit as the private sector attempts to deleverages themselves and prefer more liquid shorter-duration exposure. In addition, earning power would decrease so less money would be available for saving which is different from the Japanese scenario. It would seem that the increase in supply for treasuries (especially long-dated) would outstrip an increase in demand if we excluded the printing-press and people suddenly buying bonds after they heard of Bernanke's QE policy (even if there was not sell-off caused by a bursting of the "bond bubble"). I thought Bernanke would result to using QE eventually, but I actually expected yields to go up during the bear market rally.

I did expect the dollar to rise against the euro because it is the world's reserve currency and the world is highly levered in the world's reserve currency so this would increase the demand for dollars during deleveraging. But once the deleveraging was over, the dollar would resume its fall. In addition, the eastern european exposure to the euro would cause significant stress to the currency regime and maybe lower euro interest rates in an attempt to "stimulate" the economy. Also, I erroneously thought that the US trade deficit would narrow (it did), but the latest trade data showed that exports declined more relative to the decline in non-petroleum imports.

Of course, in the future, there is a non-trivial chance that the velocity of money would dramatically accelerate. This would cause inflation or hyperinflation (as defined by an increase in prices), not simply increases in the money supply although that might be the catalyst to trigger such an increase. Of course, inflation and hyperinflation do have a reflexive component to it, and since people believe that the Fed will cause inflation, as it did by increasing the money supply, it drives gold prices up as people seek "real" exposure, not "nominal" exposure. Gold prices do not measure directly inflation as there was positive inflation in the 90's yet lower gold prices as people wanted exposure to assets (or "delusion" in the case of most dot-coms). It measures some derivative of the demand for "real" exposure relative to "nominal" exposure which would increase during times of both deflation and in some inflationary environments. In a deflationary environment, "nominal" low-duration exposure might not offer significant interest, so the opportunity cost for holding gold would be lower. This is one reason why gold could rise in a deflationary environment.

I do not think "reflation" will "work" (which I'll define as producing "desired results" not merely producing inflation.) Even if banks become well-capitalized when the government monetizes their assets, it would not spur "enough" lending because the demand for lending would decrease. While Bernanke can lower the interest on interest-bearing assets by intervening in the bond market by buying agencies and government debt, it would not necessarily lower the "spread" or risk premium for those type of debts and consumer loans. The spread, of course, needs to compensate for the risk in the loans the banks make. I expect a situation similar to that of Japanese banks if the banks are to become well-capitalized. It seems that Bernanke's goals for QE is to lower the interest rates for consumers to get loans rather than recapitalization of banks although the latter is means for the former. I do not think QE will achieve this end. QE might not necessarily cause inflation in a given nation if it is not invested in a the country (in Japan, it might be used for "carry trades" in other currencies) or if the excess money was withdrawn from the money supply after it recapitalized the banks (which happened in Japan according to the figure here).

I still like the deflationist thesis and "Mish" (and not Peter Schiff) made me consider the merits of Austrian empirical economics, although I do not like some Austrian normative economics. Regardless of "deflation" and "inflation," this is an environment characterized by hoarding not entrepreneurialship... who knows whether it will be cash when the velocity of money is low, or real assets.

Wednesday, March 18, 2009

EVERYTHING just went to hell

I do not like USD/EUR since it past resistance and trade data doesn't seem to be helping it.

I like

SEK/EUR (25%)

SEK/JPY (30%)

SEK/ USD (15%)

CAD/EUR (20%)

AUD/EUR (15%)

Close short USD 10 year bond position at a large loss (a 47 bp move against position today)... I knew of the risks of betting against a bond market with government as a buyer (I didn't target 30 year because it has possible to have yield curve flattening and the duration risk of that position). Whatever.... I knew yields would rise without QE.

Like long GLD now... this event seems to be the catalyst to encourage more gold "investment" buying.

I like

SEK/EUR (25%)

SEK/JPY (30%)

SEK/ USD (15%)

CAD/EUR (20%)

AUD/EUR (15%)

Close short USD 10 year bond position at a large loss (a 47 bp move against position today)... I knew of the risks of betting against a bond market with government as a buyer (I didn't target 30 year because it has possible to have yield curve flattening and the duration risk of that position). Whatever.... I knew yields would rise without QE.

Like long GLD now... this event seems to be the catalyst to encourage more gold "investment" buying.

Tuesday, March 17, 2009

Exit strategies

I do not like USD/GBP anymore... bearish sentiment is already priced in at $1.40 so it does not seem the risk/reward is yet compelling. Most traders now know of the BoE policy of quantitative easing. If it rally which could happen during the global bear market rally, then I'll reconsider a short position.

EUR/USD approached 1.30... I think this is resistance, but we might see a breakout due to the current global "bear market rally." I do not think we are at the bottom yet. This bear market rally would become something shortable (perhaps in equities and commodities) in about a month or so.

I think the yen will get weaker relative to the dollar in this bear market rally... plan to close short yen/long dollar at 104-108 yen per dollar.

I'll close the short treasury trade at around 3.10-3.20% (I do not think yields will rise further in a deflationary environment) and they can fall that much during a deflationary bear market rally.

Thinking about the timing for a short copper/oil play... I am also bearish on gold too although people such as John Paulson seem to be betting on inflation (or numerous fiat currency collapses).

I am still a deflationist... I will not switch to the hyperinflationist or inflationist paradigm unless I see nominial wage increases or if the price of consumer goods such as clothes or cars go up. It is actually funny... many people are afraid of inflation because they experienced rising food and energy prices. I like the Austrian economics definition of deflation: the net expansion of money and credit, not the PPI, CPI, etc. I do not like the normative views of most Austrian economists, but those guided by an Austrian view who forecasted deflation [and that doesn't include Peter Schiff] got it right on the money. According to this view, one could have rising prices during a deflation in food, energy, or in imports (if a currency collapsed) as these prices would be affected by other things not directly related to credit and money supply such as scarcity (can happen during a deflation due to the lack of investment in farms, oil exploration, etc.) and demand in other countries. But again, what is funny about this deflationary bust and inflation... most people still fear inflation because they experienced the dark side of inflation (it can be caused by the symptoms of inflation, but it is not necessarily inflationary) in the form of rising food prices and energy prices (of course in the long run these are legitimate fears), but they do not appreciate one of the ostensibly "good" effects of inflation: nominal wage increases because that has been driven down by globalization.

Again, I do not care what the CPI or PPI (rising numbers do not falsify the Austrian deflation definition) says: we are still in deflation where people will become more thifty so the velocity of money will slow down and people will be relunctant to take on debt. The deflationary bust will last longer than people think and we will soon appreciate its negative effects.

EUR/USD approached 1.30... I think this is resistance, but we might see a breakout due to the current global "bear market rally." I do not think we are at the bottom yet. This bear market rally would become something shortable (perhaps in equities and commodities) in about a month or so.

I think the yen will get weaker relative to the dollar in this bear market rally... plan to close short yen/long dollar at 104-108 yen per dollar.

I'll close the short treasury trade at around 3.10-3.20% (I do not think yields will rise further in a deflationary environment) and they can fall that much during a deflationary bear market rally.

Thinking about the timing for a short copper/oil play... I am also bearish on gold too although people such as John Paulson seem to be betting on inflation (or numerous fiat currency collapses).

I am still a deflationist... I will not switch to the hyperinflationist or inflationist paradigm unless I see nominial wage increases or if the price of consumer goods such as clothes or cars go up. It is actually funny... many people are afraid of inflation because they experienced rising food and energy prices. I like the Austrian economics definition of deflation: the net expansion of money and credit, not the PPI, CPI, etc. I do not like the normative views of most Austrian economists, but those guided by an Austrian view who forecasted deflation [and that doesn't include Peter Schiff] got it right on the money. According to this view, one could have rising prices during a deflation in food, energy, or in imports (if a currency collapsed) as these prices would be affected by other things not directly related to credit and money supply such as scarcity (can happen during a deflation due to the lack of investment in farms, oil exploration, etc.) and demand in other countries. But again, what is funny about this deflationary bust and inflation... most people still fear inflation because they experienced the dark side of inflation (it can be caused by the symptoms of inflation, but it is not necessarily inflationary) in the form of rising food prices and energy prices (of course in the long run these are legitimate fears), but they do not appreciate one of the ostensibly "good" effects of inflation: nominal wage increases because that has been driven down by globalization.

Again, I do not care what the CPI or PPI (rising numbers do not falsify the Austrian deflation definition) says: we are still in deflation where people will become more thifty so the velocity of money will slow down and people will be relunctant to take on debt. The deflationary bust will last longer than people think and we will soon appreciate its negative effects.

Saturday, March 14, 2009

Thursday, March 12, 2009

Bear market rally?

I most definitely do not think we are close to THE final bottom, but I would remove the Russell 2000 index hedges now although it was after the recent rally, so it wasn't perfectly timed.

18% exposure in long equity is not much although I think the equity picks would underperform the indices (if I would be evaluated on a relative basis) as bank stocks might lead the rally. The risk/reward is not compelling though as I could imagine a few scenarios that could bring the equities markets lower, but I do not think we will have a retest of the new lows for awhile. SPY would probably test the 800 level in a month. I really hate establishing positions after inflection points... but I think we are about to enter a bear market rally. I do not know if we are going to best the 900 level on the S&P, but 840 seems likely.

Still bearish on the entire US bond market. Short trade does have a negative carry of about 2.90%... let's say that 2.90% is when I got bearish on 10 year treasuries. So I need about 3.20% yields to break even. I think it is just a matter of time for yields to go up as I think the money to buy these the bonds would eventually dry up. There, of course, is a risk of quantitative easing by the Fed though.

Still bearish on CHF/EUR/JPY/GBP

The CHF position did well today with a fall of 3%.

PMI ---> PM.. people will still smoke...

18% exposure in long equity is not much although I think the equity picks would underperform the indices (if I would be evaluated on a relative basis) as bank stocks might lead the rally. The risk/reward is not compelling though as I could imagine a few scenarios that could bring the equities markets lower, but I do not think we will have a retest of the new lows for awhile. SPY would probably test the 800 level in a month. I really hate establishing positions after inflection points... but I think we are about to enter a bear market rally. I do not know if we are going to best the 900 level on the S&P, but 840 seems likely.

Still bearish on the entire US bond market. Short trade does have a negative carry of about 2.90%... let's say that 2.90% is when I got bearish on 10 year treasuries. So I need about 3.20% yields to break even. I think it is just a matter of time for yields to go up as I think the money to buy these the bonds would eventually dry up. There, of course, is a risk of quantitative easing by the Fed though.

Still bearish on CHF/EUR/JPY/GBP

The CHF position did well today with a fall of 3%.

PMI ---> PM.. people will still smoke...

Tuesday, March 10, 2009

positions

I don't feel that deflation (defined as falling prices) is very likely in the Eurozone given that their economy has more wage/price rigidities.

Monday, March 9, 2009

Thursday, March 5, 2009

3/05/09

I am using this blog as a way to incoherently record my predictions on the market. Too bad I am not wealthy enough to actually put money in these positions. (I am not really going to quantify exposure to some hypothetical portfolio) I just wanted a way I could pretend to be George Soros or a global macro hedge fund manager.

Currency:

getting out of CAD/EUR and would reduce the NOK/EUR exposure. SEK still seems oversold, although it current has bad technicals. Lost on SEK/EUR although I love SEK, or maybe I only love their welfare state.

like AUD/CAD in addition to AUD/EUR

USD/GBP seems good medium term, although at $1.40 does not seem to be a good entry point. I do not think it is going up to $1.50. It might go to dollar parity so it seems to have a good risk/reward.

USD/JPY seems to have a symmetry risk reward profile now, but I would keep the position.

Still bearish in EUR.

I like the positive carry from the interest rate differentials and AUD fundamentals.

Equity:

(I would use equity indices to hedge the long positions, but in my previous blog, I wanted to make it clear that I didn't feel any need have speculative short positions on indices although there was a large sell-off recently. I was not calling bottom as I did believe that US and European equities had further to fall; it was a defensive short term position to protect against a possible rally.) Equties are expected to become sort of like junk bonds; investors expect an increasing risk premium which would be reflected by higher dividend yields (to compensate from the preceived negative sortino ratio [fear of negative volatility] from equities over the last two years). Furthermore, the market should price in less growth or no growth in a deflationary environment. An increased discount parameter for many investors would be expected because of demographic changes (older people cannot "invest in the long run" so short term gains and losses would be stressed) and also the empirical fact that equities indices are lower now than in 1997. This falsifies the conception that one should invest in an equity index for the long run

I do not think the risk/reward for the reverse arbitrage on Wyeth is no longer compelling. (I was bearish on Pfizer as opposed to more "research" based pharmas such as Merck).

Merck, Petrobras, and now I like OIH since it hit a support at $67 would be hedged with short US equity indices.

Commodities:

Getting out of gold today. Techs and especially fundamentals do not justfying any reason for holding it. I knew it was a bubble when I read that increased investor demand was increasing its price. No one will lever up to buy gold now, and again people have increased discount rates. Paying bills and debt with fiat currency is much more important that protecting "wealth" for the retail investor. Of course some wealthy people will buy it to protect their "wealth."

Fear might drive up gold in the short term, and during that rally, the risk/reward for entering a short position would be better after a rally.

The NAV of USO is low now at $400 million... doesn't seem to be many retail investors pushing up oil prices. I guess it is not a good position to short it anymore.

Debt:

A slight loss for shorting US 10 year bonds. Like fundamentals on aussie economy is doing well relative to others. Maybe short 2 year bonds (at 2.51% yield)... I think further interest rate cuts are priced in, and I do not have any reason to expect them to be cut further.

Currency:

getting out of CAD/EUR and would reduce the NOK/EUR exposure. SEK still seems oversold, although it current has bad technicals. Lost on SEK/EUR although I love SEK, or maybe I only love their welfare state.

like AUD/CAD in addition to AUD/EUR

USD/GBP seems good medium term, although at $1.40 does not seem to be a good entry point. I do not think it is going up to $1.50. It might go to dollar parity so it seems to have a good risk/reward.

USD/JPY seems to have a symmetry risk reward profile now, but I would keep the position.

Still bearish in EUR.

I like the positive carry from the interest rate differentials and AUD fundamentals.

Equity:

(I would use equity indices to hedge the long positions, but in my previous blog, I wanted to make it clear that I didn't feel any need have speculative short positions on indices although there was a large sell-off recently. I was not calling bottom as I did believe that US and European equities had further to fall; it was a defensive short term position to protect against a possible rally.) Equties are expected to become sort of like junk bonds; investors expect an increasing risk premium which would be reflected by higher dividend yields (to compensate from the preceived negative sortino ratio [fear of negative volatility] from equities over the last two years). Furthermore, the market should price in less growth or no growth in a deflationary environment. An increased discount parameter for many investors would be expected because of demographic changes (older people cannot "invest in the long run" so short term gains and losses would be stressed) and also the empirical fact that equities indices are lower now than in 1997. This falsifies the conception that one should invest in an equity index for the long run

I do not think the risk/reward for the reverse arbitrage on Wyeth is no longer compelling. (I was bearish on Pfizer as opposed to more "research" based pharmas such as Merck).

Merck, Petrobras, and now I like OIH since it hit a support at $67 would be hedged with short US equity indices.

Commodities:

Getting out of gold today. Techs and especially fundamentals do not justfying any reason for holding it. I knew it was a bubble when I read that increased investor demand was increasing its price. No one will lever up to buy gold now, and again people have increased discount rates. Paying bills and debt with fiat currency is much more important that protecting "wealth" for the retail investor. Of course some wealthy people will buy it to protect their "wealth."

Fear might drive up gold in the short term, and during that rally, the risk/reward for entering a short position would be better after a rally.

The NAV of USO is low now at $400 million... doesn't seem to be many retail investors pushing up oil prices. I guess it is not a good position to short it anymore.

Debt:

A slight loss for shorting US 10 year bonds. Like fundamentals on aussie economy is doing well relative to others. Maybe short 2 year bonds (at 2.51% yield)... I think further interest rate cuts are priced in, and I do not have any reason to expect them to be cut further.

Subscribe to:

Posts (Atom)